Read the full PDF: Click here to view the original document

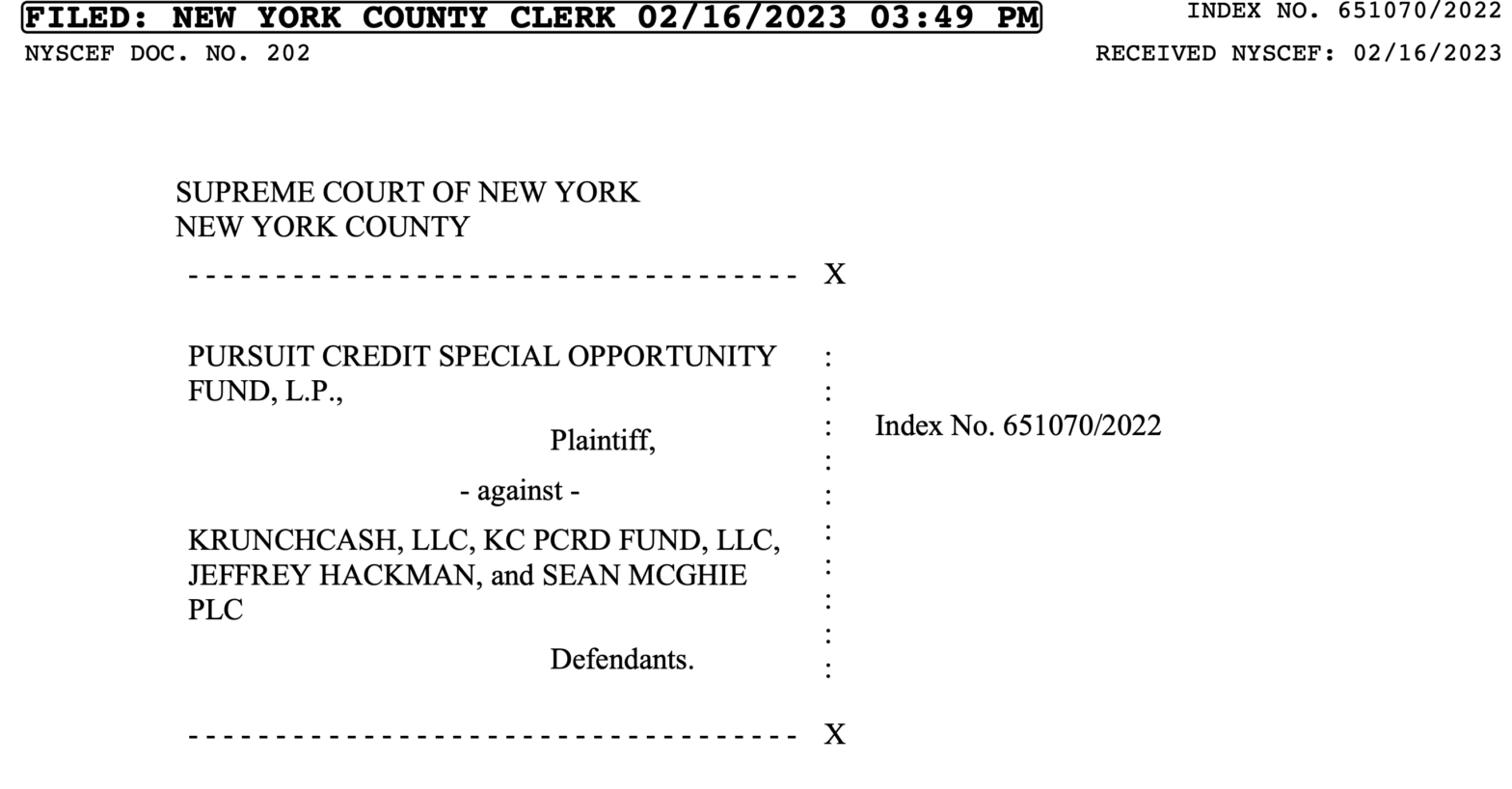

SUPREME COURT OF THE STATE OF NEW YORK

NEW YORK COUNTY

- – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – x

PURSUIT CREDIT SPECIAL OPPORTUNITY

FUND, L.P.,

Plaintiff, - against –

KRUNCHCASH, LLC, KC PCRD FUND, LLC,

KC CA FUND, LLC, and JEFFREY HACKMAN,

Defendants.

Index No. 651070/2022

RULE 19-a STATEMENT OF

MATERIAL FACTS - – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – – x

Pursuant to Commercial Division Rule 19-a, Plaintiff Pursuit Credit Special Opportunity

Fund, L.P. submits the following material facts in the record:

A. Pursuit’s Arrangements with the KrunchCash Entities

- The KrunchCash Entities were specialty finance entities. (Cohen Aff. ¶¶ 2, 8, 107.)

- KrunchCash was an investor into legal funding assets, including law firm, plaintiff,

and medical lien funding, and advances backed by pharmaceutical receivables (“Advances”).

(Ex. 3 (KrunchCash Dep. 1/8/2025) at 13:01–16:25; 148:13–149:23; Ex. 1 at 49:14–51:16.) - Pursuit invested with KrunchCash and KC PCRD through 2021. (Cohen Aff. ¶¶ 2,

71-78, Ex. 3 at 13:01–16:25.) Pursuit invested into KrunchCash-related opportunities through

revenue-sharing arrangements wherein Pursuit would hold the right to revenues from particular

Advances. (Cohen Aff. ¶¶ 4-11, Ex. 3 at 14:20–15:6; 42:3–7.) - From 2015 through early-2018, Pursuit and KrunchCash were parties to an Investor

Funding Agreement dated April 2015 (the “Original IFA,” as amended) and a Purchase Agreement

dated September 2017. (Ex. 7 (Investor Funding Agreement dated 1/15/2015); Ex. 8 (Purchase

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

1 of 32

2

Agreement dated 9/29/2017); see also Ex. 1 at 26:9-27:4, 46:10-14 (authenticating Original IFA)

and 116:14-117:3, 117:18-118:9 (authenticating Purchase Agreement); Ex. 3 at 15:4–24.) - On April 10, 2018, Pursuit and KC PCRD entered into the Amended and Restated

Funding Agreement (the “Amended IFA”), which supplanted the Original IFA. (Ex. 9 (Amended

IFA dated 4/10/2018); see Ex. 1 43:7-44:22 (authenticating Amended IFA).) - The claims at issue here pertain to Pursuit’s investment from the date of the

Amended IFA through November 26, 2019 (the “Investment Period”). (Ex. 10 (Expert Report of

Graham Rogers dated 5/22/2025) ¶¶ 61–64.) - With the Amended IFA, KrunchCash created a new entity—KC PCRD—to hold

the monies that Pursuit invested. (Ex. 9; Ex. 1 at 22:13–18.) - The Amended IFA contemplates that KC PCRD would make Advances to and recollect monies from third-party Recipients. (See Ex. 9 § 3, Cohen Aff. ¶¶ 6-11.)

- In practice, KrunchCash would receive investor funds, route those funds back to

KC PCRD, and then KC PCRD would transfer monies back to KrunchCash. KrunchCash would

then make Advances and receive repayments from Advances from a KrunchCash account that

Hackman referred to as the “cash management account,” and KrunchCash would then remit

Pursuit’s portion of Advances back to KC PCRD. (See Ex. 1 at 65:16–68:21; Ex. 4 (KrunchCash

Dep. 1/9/2025) at 16:08–19:24; Cohen Aff. ¶¶ 8-9.) From the KC PCRD account, monies could

be distributed to Pursuit or, as was the case here, were consistently reinvested into additional

Advances. (See id.) - Paragraph 6 of the Amended IFA contains the waterfall pursuant to which Pursuit

and KC PCRD would split proceeds from Advances:

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

2 of 32

3 - Allocations and Disbursements. The proceeds from each

Advance provided with the Investor Funding will be allocated and

disbursed as follows:

(i) First, the amount repaid by the funding recipient will be

deposited into the Bank Account1 (“Repayment Amount”).

(ii) Second, the Advance will be deducted from the Repayment

Amount and left in the Bank Account to be re-advanced.

(iii) Third, the difference between the Repayment Amount and the

Advance (net of the Servicing Fee payable to Company pursuant to

Section 4) will be allocated and disbursed as follows: (A) Fifty

percent (50%) of the proceeds will be allocated and disbursed to

Investor; and (B) Fifty percent (50%) of the proceeds will be

allocated and disbursed to Company [KC PCRD]. Company will

disburse such proceeds no more than once per calendar month to the

extent of cash available.

(Ex. 9, Ex. 1 at 76:15–22.) - Thus, per Paragraph 6(i) of the Amended IFA, the “Repayment Amount,” i.e., the

principal advanced using Pursuit’s capital and repaid to KrunchCash, was to be repaid into the

dedicated KC PCRD bank account as a first step for safekeeping. (See id.) - Paragraph 6(iii) contemplates a profit-share, calculated as 50% of the “Repayment

Amount” minus the “Advance,” to Defendants. (Id., Cohen Aff. ¶¶ 10-11.) - There is no upfront “Servicing Fee” and the Amended IFA explicitly states that the

“Servicing Fee” is equal to “zero percent (0%)[.]” (Ex. 9 § 4, 6(iii).)

B. The Advances - Pursuit’s investments were supposedly tied to and backed by proceeds from the

underlying claims that served as collateral to KrunchCash’s Advances to third-party recipients

(“Recipients”). (Ex. 9 § 2, 3.)

1 The Amended IFA defines “Bank Account” as the KC PCRD account.

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

3 of 32

4 - Pursuit was granted a first-lien security interest in all proceeds from Advances it

funded, and KrunchCash agreed to assign all “right, title and interest” in all proceeds received

from Advances to KC PCRD for such purpose. (Id. § 7, 2.) - The “Resnick” or “Maryland” Advances were a series of Advances to related

personal injury firms The Law Offices of Jonathan S. Resnick LLC (owned by Jonathan Resnick)

and The Law Offices of Perry A. Resnick (owned by Perry Resnick, son of Jonathan Resnick), and

the Law Offices of Louis Glick (collectively the “Resnick Firms”). (Ex. 1 at 146:01-152:13.)

Additionally, there were Advances made to healthcare provider American Wellness Health Center

Inc., a medical provider to clients of the Resnick Firms (collectively, the “Maryland Firms”). (See

Ex. 1 at 52:11-17.) - Defendants represented that the Advances by KrunchCash to the Resnick Firms

were secured and repaid by a portion of each firm’s one-third contingency fee and entitlement to

recoup out-of-pocket expenses from underlying litigations. (See Ex. 1 at 29:07–21; 35:19–36:04,

52:02–53:19, Cohen Aff. ¶¶ 18-21.) The anticipated proceeds from the Resnick Firms’ injury cases

were under $20,000 per litigation and averaged around $5,000. (Ex. 1 at 150:05–20; Ex. 23 (Perry

Resnick Dep. 3/28/2024) 15:08-15.) The amount the Resnick Firms were entitled to receive as a

contingency fee was a percentage of the total proceeds, typically around 33 percent if no lawsuit

was filed, and 40 percent if an action was commenced. (Ex. 23, 15:21-16:05.) KrunchCash

purported to provide several forms of funding to the Resnick Firms including pre-settlement,

expense, post-settlement, and medical funding. (Ex. 11 (KrunchCash Funding Summary

10/12/2017), Ex. 1 at 150:05–162:17.) - Defendants represented that KrunchCash’s entitlement from the Resnick Firms was

the amount of the Advance—i.e., the principal funded to the firm—plus a “Use Fee.” (Ex. 1 at

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

4 of 32

5

217:8-17; 219:7-220:8, 35:19-36:4.) The “Use Fee” was an amount equal to 4% per month from

the time the monies were funded, subject to a six-month minimum equal to 24%. (See id.) At least,

these were the terms represented to Pursuit when Hackman described the nature of the Advances.

(Ex. 11.) - Thus, based on the waterfall described above, if KrunchCash successfully

recollected an Advance that had accrued a minimum six-month “Use Fee” then Pursuit would

receive 112%—equal to return of the Advance (100%) plus half of the Use Fee (12%)—and the

KrunchCash Entities would receive 12%—equal to the other 50% of the Use Fee. (Ex. 1 at 29:7–

21, 219:7–220:8, 164:5–165:4, 242:18–243:5; 294:4–295:9, Cohen Aff. ¶ 22.) - The “LB Pharma” Advances were monies KrunchCash funded to a Texas-based

pharmaceutical business, LB Pharma and its affiliates. (Ex. 1 at 52:18–24; Ex. 3 at 14:1–19, Ex.

12 (Email Hackman to Pursuit 10/25/2018).) Defendants represented that the receivables to

LB Pharma were adjudicated pharmaceutical insurance claims that would be expected to pay off

in 30-45 or 45-60 days. (Cohen Aff. ¶¶ 23-25, Ex. 12, Ex. 3 at 57:8–17, 69:16–70:4, 162:12–25,

164:3–7, 165:1–3.) - Pertinently, Pursuit also provided $872,000 in capital to Defendants to advance to

a Connecticut-based law firm, Berkowitz Hanna LLC (“BH”), secured by that firm’s receivables.

(See Ex. 4 at 259:24–261:19.) - KrunchCash claimed to have invested in other Advances, unrelated to Pursuit, such

as Advances secured by ex-NFL players’ recoveries from the litigation against the NFL (the “NFL

Advances”). (Ex. 4 at 189:2-4; Ex. 1 at 42:24–43:6, Ex. 4 at 189:2–4.) Defendants refused,

however, to produce information to substantiate other Advances. (Docs. 655, 735, 717 (Motion

Seq. 18).)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

5 of 32

6

C. Defendants’ Representations Concerning the Advances and Ledgers - Hackman shared with Pursuit a spreadsheet “Ledger” that Hackman manually

created and maintained on Microsoft Excel. (See Ex. 1 83:16–88:2, Ex. 4 at 106:12–17; 156:16–

22; 157:16–23, Cohen Aff. ¶¶ 29-33, Ex. 13 (Pursuit Ledger).) Hackman had a trusting relationship

with Pursuit’s manager, Mitchell Cohen (“Cohen”). (Cohen Aff. ¶ 27.) The two spoke multiple

times weekly concerning the Advances, and Hackman attempted to befriend Cohen. (See id. ¶¶

27-30.) - The Ledger reflected the supposed balances and performance of the Advances on

an overall and claim-by-claim (i.e., plaintiff-by-plaintiff) level. (Ex. 1 at 83:16–88:2; Ex. 4 at

100:2–102:19.) The Ledgers then tabulate the monies invested by Pursuit into the KrunchCash

Entities, supposedly funded by KrunchCash to the end-Recipients using Pursuit’s capital, and

supposedly collected, along with the “Use Fee”, from Recipients. (Ex. 1 83:16–88:2, Ex. 4 at

106:12–17, 200:12–202:16 (the parties “relied” on the Ledger to monitor performance).) The

Ledger then tracks the “waterfall” and presents calculations of Pursuit’s investment balance and

Defendants’ profit-share. (Ex. 1 83:16–88:2, See Ex. 13, Ex. 1 at 71:12–77:2, 83:16-88:2, 132:8–

133:14, Ex. 4 at 100:2–106:17.) The Ledgers also provided various performance-related data

concerning the Advances, including the date of funding, date of repayment, and duration of each

claim. (Ex. 1 at 83:7–24.) - Hackman shared the Ledger live through a cloud account. (Ex. 1 at 84:19–85:3,

231:23–234:25.) Though the Ledger was cloud-based, Pursuit’s principals would periodically

download and date-lock the Ledger for internal record-keeping purposes. (Cohen Aff. ¶ 29, Ex.

13.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

6 of 32

7 - Hackman and the KrunchCash Entities represented, in the Ledger and throughout

Pursuit’s investment and reinvestment, information concerning the Resnick Advances. (Ex. 1 at

231:23–234:25.) Such representations included that:

- Each Advance on the Ledger reflected new monies that KrunchCash

actually advanced to the Recipient in cash based on the Recipient’s new

need for monies. (Ex. 1 at 231:23–234:25, 225:23–226:16.) The Ledger

represented that, during the Investment Period, KrunchCash advanced over

$45 million to the Maryland Recipients. (Ex. 13, at Tabs LAW.LG,

LAW.PR, PIP, Post, and LOP (sum of “Gross” amounts funded on or after

Apr. 10, 2018); Ex. 4 at 106:9–11 (over $63 million over time).) - Claims reflecting “collected” values on the Ledger were successfully repaid

by the Maryland Recipients from settlement proceeds. (Ex. 10 ¶ 31.)2 The

Ledgers reflected that, during the Investment Period, the Maryland

Recipients repaid $7.2 million to KrunchCash. (Id. ¶ 158.) - When Pursuit dedicated capital to a particular Advance, each of the claims

within that Advance was unencumbered, such that Pursuit was the only

investor with an interest in that receivable. (Cohen Aff. ¶ 34, Ex. 9 § 2, 7;

Ex. 1 at 29:7–21, 35:19–36:4).) - Each Advance was collateralized 2-to-1, meaning that for each “claim”

backing an Advance, there was another unencumbered claim handled by the

Resnick Firm that could serve as replacement collateral. (See Ex. 2 at

472:2–6, Cohen Aff. ¶ 34, Ex. 1 at 29:7–21, 35:19–36:4.) This gave Pursuit

comfort that there was value in the Resnick Firms beyond the claims that it

was funding. (Cohen Aff. ¶ 34.)

- Defendants also made representations concerning the LB Pharma Advances, which

included that:

- The Advances were being made to pharmacies that held portfolios of

adjudicated—i.e., resolved—reimbursement claims that would be repaid

within 30-45 or 45-60 days. (See Ex. 3 at 18:6–24, Ex. 4 at 162:12–25,

164:3–165:3; 69:16–70:4, Ex. 12.)

2 There is one exception wherein, in the month prior to execution of the Amended IFA,

Pursuit permitted Hackman to sell one portfolio of receivables to which Pursuit had an interest to

another then-unknown investor for $1 million. (Cohen Aff. ¶ 34.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

7 of 32

8 - Advances were being repaid on a timely basis—i.e., each “tranche” and

“claim” within than tranche—was repaid profitably from insurance

proceeds. (Ex. 4 at 161:17–19.) - When Pursuit dedicated funding to an LB Pharma Advance, KrunchCash

was actually funding such amounts to LB Pharma in cash. (Ex. 14–16 (Text

Messages Hackman and Cohen 9/9/2018, Text Messages Hackman and

Cohen 8/22/2018, Text Messages Hackman and Cohen 10/19/2018).) The

Ledger represented that more than $41 million had been advanced to LB

Pharma. (Ex. 4 at 105:20–106:11 (Q: Does the $41 million represent actual

funds out to the advance recipient? A: Yes.).) - LB Pharma had repaid approximately $35.5 million in total before

defaulting. (Ex. 13, TAB “RX” (showing amounts “Collected”).)

- Hackman provided read-only access to Pursuit to the bank account held in the name

of KC PCRD. (Cohen Aff. ¶ 36.) Each time that he reflected claims as “collected” on the Ledger,

Hackman moved monies to the KC PCRD account to mirror such transactions—thus giving the

illusion that cash was being collected. (Id., Compare Ex. 13 (Ledger) at “Register” Tab with Ex.

35-1 (Bank Statement).) But, as discussed below, Pursuit is now aware that the cash that Hackman

temporarily deposited into the KC PCRD account, and which Hackman quickly transferred back

to KrunchCash for supposed reinvestment, was not cash actually received from the end-Recipients.

(Ex. 10.) - Hackman testified he had unfettered authority, power, and discretion to invest

Pursuit’s capital however he wished. (Ex. 1 at 39:32–42:23.) Pursuit did not need to agree on how

funds would be reinvested “because Pursuit had no input on the business per the agreement. No

participation.” (Ex. 1 at 74:5–75:7.) There were “no limits” on Hackman’s latitude, including

theoretically, gambling Pursuit’s money in Las Vegas. (Ex. 1 at 74:5–75:7, 108:18–109:16.) - Pursuit invested and reinvested based on Hackman’s representations in the Ledgers

and otherwise as to the nature of the Advances and Defendants stewardship of Pursuit’s funds. As

of the date of the Amended IFA, Pursuit had invested $2.8 million with KrunchCash. (Ex. 9 § 1,

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

8 of 32

9

Ex. 13, Ex. 10 ¶¶ 21.) Following execution of the Amended IFA, Pursuit invested an additional

$8.2 million—bringing Pursuit’s total investment to approximately $11 million. (Ex. 9 § 1, Ex. 13,

Ex. 10 ¶¶ 192.) Hackman made some distributions to Pursuit—which Pursuit now understands to

have been false-profit distributions—such that Pursuit’s net out-of-pocket investment was $7.16

million. (Ex. 9 § 1, Ex. 13, Ex. 10 ¶¶ 191-192.) - Based on the represented success of the LB Pharma Advances, specifically, Pursuit

invested approximately $8 million in new cash into KC PCRD for LB Pharma between July 2018

and April 2019. (Cohen Aff. ¶ 40; Ex. 10 ¶ 187.) In the summer and fall of 2018, Hackman spent

considerable effort inducing Pursuit to invest additional capital. (Cohen Aff. ¶¶ 41-45; Ex. 1 at

334:13-336:4; Ex. 38 (Text Messages 8/22/2018); Ex. 14; Ex. 15; Ex. 16.) Hackman travelled to

New York and met with Pursuit’s two managers and one of its limited partners to solicit new

investment. (Cohen Aff. ¶ 41; Fergang Aff. ¶¶ 8-9, Ex. 1 at 334:13-336:4, Ex. 38, Ex. 14, Ex. 16.)

Hackman represented that the LB Pharma opportunity required nearly $4 million in new cash

funding based and warned that, if Pursuit did not act quickly, another investor might seize the

opportunity. (Cohen Aff. ¶¶ 41-45; Ex. 1 at 334:13-336:4); Ex. 38 (“Need a large commitment

from [substantial investor] so [Pursuit] can stay in the game[.]”); Ex. 14 (affirming that LB Pharma

was seeking $3.3 million and “it is going to get bigger every week thereafter” and that Hackman

“need[ed] the investors to keep up with me”); Ex. 16.) When Pursuit’s limited partner, enthralled

by the false returns that Hackman had been indicating on paper, inquired if Hackman could scale

his Advances, Hackman responded that LB Pharma had endless inventory that KrunchCash could

fund, limited only by Pursuit’s willingness to invest new capital. (Fergang Aff. ¶¶ 10-16, Cohen

Aff. ¶¶ 42-46.) Based on such representations, Pursuit wired a new tranche of $3.25 million in

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

9 of 32

10

cash, adding to the other monies Pursuit had already invested in LB Pharma. (Ex. 1 at 334:13-

336:4).) - As of December 31, 2018, Pursuit’s investment balance as reflected on the Ledger

was $9.5 million. (Ex. 17 (Email Hackman to Pursuit 6/4/2019) (“As of 12.31.18 PCRD investor

funding account balance was $9,510,000.”); Ex. 4 at 183:1–183:10.) - The Ledgers represented that, based on KrunchCash’s supposed successful

recoveries from Advances, that they were entitled to $2,935,060.88 in profit-share compensation

during the Investment Period. (Ex. 13.) - Hackman also issued bulk advances to the Maryland Recipients for “litigation

expenses” and advances supposedly backed by “Letters of Protection”, however there are no

corresponding transfers to the Maryland Recipients evidencing this. (Compare Ex. 13 (Ledger) at

“LOP” Tab (representing $300,000 purportedly advanced against Letters of Protection for 1500

cases on 5/11/2018) and Ex. 34 (Signal Ledger) at “EXP” Tab (representing $300,000 purportedly

advanced for medical expenses against 1000 cases on 5/11/2018) with Ex. 35-2 (KrunchCash Bank

Statements) May 2018 at pp. 153-155 (showing no corresponding KrunchCash advance to the

Maryland Recipients on or around 5/11/2018, but a transfer from KC-PCRD’s account to

KrunchCash of $300,000 on 5/15/2018). According to the Ledger, $1.1 million in “bulk” advances

were funded using Pursuit’s investment capital, and another $2.6 million in “bulk” advances were

either funded or purchased using Signal Fund’s investment capital, each time without a

corresponding transfer to the Maryland Recipients. (See Ex. 13 (Ledger) at “LOP” Tab, F:5 and

Ex. 34 (Signal Ledger) at “EXP” and “MED” Tabs, F:7; see generally Ex. 35-2 (KrunchCash’s

Bank Statements).)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

10 of 32

11

D. The Default Actions and Discovery of Other Investors - In 2019, matter shifted. Pursuit attempted to redeem some of its capital, but

Hackman denied Pursuit such right. (Ex. 18 (Email Hackman to Pursuit 6/4/2019); Ex. 19 (Email

Cohen to Hackman 8/8/2019).) - In mid-2019, Pursuit also attempted to conduct a financial “review” of Pursuit’s

investment, so that Pursuit could substantiate the supposed success of its investment as set forth in

the Ledgers. (Ex. 20 (Email Hackman to Pursuit 11/13/2019), Ex. 4 at 183:21–186:19.) Pursuit

was unable to do so because, when Pursuit’s outside accountant sought access to bank records for

the “cash management” account in the name of KrunchCash—to tie out actual cash flows between

KrunchCash and the Advance recipients—Hackman refused to provide sufficient data. (Ex. 20;

Ex. 4 at 183:21–186:19; Doc. 110 (Parzygnat Affidavit) ¶¶ 4-6.) No review was ever completed

on Pursuit’s investments (or the KrunchCash Entities, which was never the subject of the review

in any event) because KrunchCash would not provide such records. (See id.) While Pursuit had

access to the KC PCRD bank statements, until such records were compelled through discovery in

this action, Pursuit never possessed KrunchCash’s bank statements. (Cohen Aff. ¶ 55.) - Instead, Hackman revealed that KrunchCash had become a party to various

litigations with the Resnick Firms and with LB Pharma (the “Default Actions”). (Ex. 3 at 84:2–8.)

The Default Actions sparked new issues among the parties. - Hackman explained that that Resnick Firms had abruptly stopped making

repayments to KrunchCash, and insisted that the Resnicks—Jonathan Resnick, in particular—had

stolen millions that KrunchCash had funded. (Ex. 21 (Hough Dep. 6/7/2024) at 162:19–163:24.)

Hackman could not explain, however, where Jonathan Resnick supposedly directed these monies.

(Ex. 21 at 210:7–212:13; Ex. 29 (Overview of Resnick Default Actions to Signal); Ex. 30

(Overview of Resnick Default Actions to Pursuit).) Hackman claimed that there were thousands

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

11 of 32

12

of missing files at the Resnick Firms that could not be located. (Ex. 29; Ex. 30.) Though Hackman

initially suppressed such facts from Pursuit, the Recipients asserted—and maintain today—that

Hackman falsely inflated the amounts funded to the Recipients. (See Ex. 22 (Jonathan Resnick

Dep. 3/27/2024) at 146:1-147-5, Ex. 23 at 50:2-21.) - With respect to LB Pharma, Hackman explained that LB Pharma was entangled in

a convoluted audit and that repayments would resume once LB Pharma surpassed the obstacle.

(Cohen Aff. ¶ 59.) - Initially, Defendants aggressively pressed Pursuit to invest new extra-contractual

capital to support legal fees and KrunchCash’s operational expenses—including compensation to

Hackman—as the Default Actions progressed. (Ex. 2 at 487:9–18.) - Through these discussions, Defendants divulged that there were in fact (at least)

three investors—Pursuit, Signal Funding LLC (“Signal”), and KrunchCash (purportedly using

KrunchCash’s capital)—that had invested alongside one another into the Resnick Advances.

(Ex. 21 at 158:15–161:19; Ex. 24 (Email Hackman to Pursuit 4/1/2020) (“As discussed, there are

3 investors who have provided funding to the Resnicks, and 2 investors who have provided funding

to LB Pharma.”).) Hackman insisted that each of Pursuit and Signal contribute additional capital

to support the Default Actions, falsely stating that the other investor had already funded. (Ex. 21

at 216:17-217:10; Ex. 24.) - This was a red flag. Neither investor knew that the other had invested in the same

Advances. (Ex. 21 at 90:9-15, 109:18-112:9, 158:15–161:19, 151:23–152:24, 114:10–13, 78:4–9;

Cohen Aff. ¶¶ 61-65.) Pursuit and Signal each sought clarification as to how proceeds from the

Advances and/or Default Actions would be reconciled and distributed—as between three intercreditors—were they to be received. (Ex. 27, Ex. 21 at 124:11-125:22, 206:17-210:3; 124:11-

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

12 of 32

13

125:22; Cohen Aff. ¶ 64.) Each questioned how the Advances could realistically be parsed or

prioritized. (Id.) When Pursuit attempted to contact Signal to discuss these issues, Hackman lashed

out and threatened to sue Pursuit based on nonsensical confidentiality concerns. (Ex. 56.) The

revelation of three inter-creditors suggests irreconcilable competing liens over the same

collateral—i.e., double-pledging. (Ex. 10.) - Defendants’ representations about the Default Actions and multiple intercreditor

issues raised deepened red flags concerning the monies KrunchCash had funded to the Resnick

Firms. The Pursuit Ledger stated that, immediately prior to the Resnick Firms’ purported breach,

KrunchCash had outstanding Advances of approximately, $4.1 million (and $45 million funded

over the Investment Period), an amount that could have reasonably substantiated the coverage

ratios Pursuit understood to exist. (Ex. 13; Ex. 10 ¶¶ 34, 67, 97.) However, Hackman now claimed

that Signal and Hackman had an outstanding additional $13 million to the Resnick Firms—above

Pursuit’s amount—such that the total amount invested was $17.5 million. (Ex. 25 (Email Hackman

to Pursuit 3/20/2020).) By all accounts, Hackman’s representation of 2-to-1 collateralization was

false, and neither Pursuit nor Signal could have a first lien to the same receivables. - Likewise, contrary to Defendants’ representation that Pursuit was the only investor

in LB Pharma, Hackman also divulged that there was an additional investor in LB Pharma, thus

creating an irreconcilable double-pledging of the LB Pharma proceeds, as well. (Ex. 26 (Email

Hackman to Pursuit 3/20/2020).) - In April 2021, Pursuit sent a demand letter, seeking to satisfy the foregoing

concerns, so that Pursuit could continue protecting its investment with ample guardrails. (Ex. 27

(Ltr. Pursuit to Hackman 4/16/2021).) Defendants responded with a scathing attack. (Ex. 28 (Ltr.

Defendants to Pursuit 5/8/2021).) Instead of answering Pursuit’s request for an accounting,

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

13 of 32

14

Defendants gaslit Pursuit. (See id.) Because neither Pursuit nor Signal had access to the

KrunchCash bank account records—from which Hackman made and collected the Advances—

neither investor could verify the monies funded or owed. (Ex. 21 at 139:18–140:2, 145:22–146:10,

148:9–149:6.) Nor did Pursuit or Signal have access to the other’s Ledger showing the claims to

which each had an interest. (Ex. 1 at 272:24–273:8.) - Defendants became increasingly aggressive. After originally explaining that to

Pursuit that the Resnick Firms and LB Pharma owed and had stolen millions—and that Pursuit

should invest to protect such investment—Defendants threatened to scuttle the Default Actions in

bad faith if Pursuit did not capitulate. (Ex. 20; Ex. 24; Ex. 26; Ex. 30; Ex. 25.) - As Pursuit pressed, Pursuit learned that Defendants had been collecting and

intercepting receivables in which Pursuit had an interest. Defendants refused to turn over

approximately $270,000 from the BH Advance (Ex. 1 at 258:10–268:25, Ex. 31 (Ltr. to Pursuit

1/11/2022)) and refused to pay $275,000 indisputably owed on unrelated Advances. (Ex. 18.)

Defendants admitted Hackman had collected monies throughout the Default Actions, including

approximately $700,0003 by intercepting funds from an LB Pharma insurance payor (EPIC) and

approximately $2.5 million in additional collections from the Resnick Firms, but Hackman refused

to fully pay over such funds to Pursuit. (Ex. 32 (Payment EPIQ to KrunchCash 1/16/2020).)

Instead, Defendants began claiming that Pursuit waived its right to any proceeds based on their

refusal to blindly fund more monies to Defendants. (See Ex. 1 at 99:5–100:23.)

3 Upon learning that KrunchCash had intercepted these funds, Pursuit was able to negotiate a

partial repayment from the $700,000 intercepted from EPIC. (Cohen Aff. ¶ 75.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

14 of 32

15 - Ultimately, Hackman cut off Pursuit’s and Signal’s access to the shared cloud

accounts, the Ledgers, and the accounts to each investor’s dedicated entity (KC PCRD or KC SF).

(Ex. 21 at 33:3–35:22, 137:6–139:17, Cohen Aff. ¶¶ 77-78.)

E. Rogers’ Early Identification of Churning, Double-Pledging, and Siphoning of Funds

to KC CA - Early in this action, Pursuit and counsel engaged Graham Rogers of Eisner

Advisors Group, LLC (“Rogers”) to examine Defendants’ records. (Doc. 91.) - Rogers analyzed available data, including the Pursuit Ledger and the ledger that

Defendants provided to Signal (the “Signal Ledger”), which Signal produced in discovery. (Ex. 10

¶¶ 42, Ex. 34 (Signal Ledger); see Ex. 21 at 125:23-126:21 (authenticating Signal Ledger).) Rogers

observed substantial overlap between the claims listed on the Pursuit and Signal Ledgers,

indicative of churning and double pledging. (See id. ¶¶ 121-125, 147-164.) Specifically, there was

a pattern wherein:

First, KrunchCash sold proceeds from one Advance to Pursuit and

reflected the principal and “Use Fee” charged to the Resnick Firm

on the Pursuit Ledger. For example, the Pursuit Ledger would reflect

an $800 Advance plus a $192 minimum repayment amount, which

included the embedded (24%) “Use Fee.”

Second, KrunchCash would sell that claim from the Pursuit Ledger

to the Signal Ledger and reflect the Pursuit Ledger as paid off in the

“collected” column. This gave Pursuit the impression that a claim

was successfully repaid by the Resnick Firm and triggered

KrunchCash’s entitlement to 50% of profit share. But, in fact, the

claim was being sold from one ledger to the other without any actual

cash flow from the Resnick Firm.

In this step, the Signal Ledger would reflect an artificially increased

Advance amount above the $992 (e.g. $1,000) although, as is now

clear, there is no evidence that additional monies were funded to the

Resnick Firm. The Signal Ledger would then reflect a minimum

repayment amount that embedded an additional 24% “Use Fee”

(e.g. $1,240) supposedly owed by the Resnick Firms.

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

15 of 32

16

Third, KrunchCash would then engage in a third similar transaction

following the pattern above, reflecting the same false resolution of

the claim on Signal’s Ledger, and a corresponding artificial increase

in lending basis to the Resnick Firm as the claim was transferred to

Pursuit’s Ledger as a post-settlement Advance. As discussed below,

this third transaction often occurred after the underlying personal

injury lawsuit had resolved.

(Id. ¶¶ 123-124.) - The Court granted Pursuit’s motion to compel access to KrunchCash’s and KC

PCRD’s records at First Citizens Bank. (Doc. 115.) - Rogers’ early analysis of those records indicated that Defendants had

surreptitiously transferred over $5 million to KC CA, another Hackman entity. (Doc. 214.)

Hackman resisted production of the KC CA records, but explained that he was entitled to use such

proceeds because such account was a repository for his profits. (Ex. 33 (KC CA Interrogatory

R&O 7/31/2023); Ex. 1 at 76:22–79:21.) Pursuit ultimately obtained such records, which Rogers

then analyzed.

F. Rogers’ Final Report Demonstrates Fraud - In May 2025, Rogers submitted his final report. (See Ex. 10.) In addition to

analyzing the KrunchCash Entities’ bank statements and the Ledgers, Rogers analyzed “Settlement

Sheets” shared by the Resnick Firms with Hackman which showed each law client’s settlement,

date of accident, date of resolution, and the distribution proceeds, which Pursuit obtained in

litigation. (See id. ¶¶ 42, Exs. 35-1–35-7 (Bank Statements), Ex. 36-1–36-5 (Compilation of

Settlement Sheets).) Rogers conducted (1) a “Transaction Reconstruction” to normalize and

analyze the bank statements, (2) a “Forensic Analysis” to determine whether Defendants’ data met

forensic patterns of a Ponzi scheme, false entries, churning, double-pledging, and other fraud, and

(3) calculations of damages. (See id. ¶¶ 45-100, 111-189, 190-198.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

16 of 32

17

G. The Transaction Reconstruction Demonstrates Commingling, Misappropriation,

Use of Investor Funds for Personal Purposes, Missing Monies for Advances, and

that New Investors’ Monies were Used to Satisfy Debts to Previous Investors - In the Transaction Reconstruction, Rogers analyzed bank accounts in the name of

KrunchCash, KC PCRD, KC CA, and KC SF Fund LLC (“KC SF,” the entity Hackman devised

for Signal). (See id. ¶¶ 47-59.) Hackman confirmed that no bank accounts other than those

analyzed by Rogers, including the KrunchCash cash management account, were used to fund

advances sent to LB Pharma or the Maryland Recipients and that all relevant funds were tracked

through KC PCRD’s bank statements and the KrunchCash cash management account statements.

(Ex. 1 (KC CPRD Dep. 7/17/2024) at 347:18–348:10.)

i. Investor Funds – Inflows and Outflow - Rogers determined that three investors—Pursuit, Signal, and 1939 Capital, LLC

(“1939”)—invested during the “Investment Period.” (See id. ¶¶ 61-64.) Collectively, those

investors funded $14.65 million into the KrunchCash Entities, and $5.11 million was returned to

investors, for a net of $9.536 million invested. (Id. ¶¶ 62-63.) Additionally, as of the date of the

Amended IFA, Pursuit had a balance of $2.8 million and, one month prior, Signal invested $1.48

million. (See id. ¶¶ 63.) Thus, there was nearly $14 million of net new capital injected into the

KrunchCash Entities during the Investment Period. (See id.)

ii. Payments to Previous Investors - During the same period, in addition to remitting approximately $5.11 million to

present investors, the KrunchCash Entities remitted several million dollars to at least three prior

investors. (See id. ¶¶ 65-66.)4

4 Hackman repaid in excess of $5 million to prior investors during and immediately prior to the

Investment Period. (Ex. 10 ¶ 65, n.56.) Like Pursuit, Hackman owes millions in unpaid

receivables and cut off transparency. (E.g., Ex. 54 (Email with Xynergy 1/14/2025).)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

17 of 32

18

iii. Commingling/Transfer of Investor Funds - Rogers determined that although Pursuit, Signal, and 1939 had its own Hackmanowned entity—KC PCRD, KC SF, and KC 1939—Hackman commingled the vast majority of

monies in the account in the name of KrunchCash, and not in the investor entities. (See id. ¶¶ 67-

72.) Monies were momentarily moved to the special-entity account (KC PCRD, in the case of

Pursuit)—to give the illusion that of repayments and profits—but those monies did not correspond

to actual repayments and Hackman immediately transferred such funds back to the KrunchCash

account. (See id.)

iv. Misappropriation of Investor Funds - Rogers determined that Defendants used investor funding for non-Advance

purposes. (See id. ¶¶ 73-88.) The Amended IFA provides that Pursuit’s monies were only to

“provide Advances,” (Ex. 9 § 2, 5, 6), that Defendants’ compensation was the 50% profit-split (id.

§ 5-6), and that the “Servicing Fee” was “zero.” (Id. § 4.) Thus, the only monies legitimately

available to fund Defendants’ operations were profit-shares from Advances or Defendants’ own

capital. - Rogers analyzed (1) the amounts Defendants deployed on uses other than

Advances, such as non-Advance overhead of KrunchCash or Hackman’s personal expenses, and

(2) compared those figures to potential legitimate sources of funds. (Ex. 10 ¶¶ 76-77.) - Legitimate sources of capital include legitimate profit-shares from Advances and

independent retained capital. (Id. ¶¶ 80-81.) The cash across the KrunchCash Entities as of the

Amended IFA date was $1.1 million, which Rogers conservatively assumed to be the maximum

retained earnings (although there is evidence that there were no retained earnings at all). (See id.

¶¶ 81.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

18 of 32

19 - As for Advance profits, during the Investment Period, there was a net outflow of

$1.62 million from the KrunchCash Entities to the Maryland Recipients and a net outflow of

$4.947 million across all Advances; thus there were no cash profits. (See id. ¶¶ 83.) As a different

measure, as a check, Rogers performed a similar calculation of alleged profits by examining the

profit-shares as claimed on the Ledgers, assuming for purpose of the analysis that such Ledgers

accurately reflected profits (though they do not). (See id. ¶¶ 84-87.) Under both calculations, there

were insufficient legitimate sources—retained capital and profits—to fund Defendants’ expenses

incurred during that period. (See id.) Accordingly, Rogers concludes that, because there are

insufficient legitimate sources to support Hackman’s non-Advance spending, but over $14 million

of new capital received from investors during the same time period, Defendants misappropriated

Pursuit, Signal, and 1939 investor funds for such non-Advance uses. (See id. ¶¶ 87-88.)

v. Use of Funds for Personal Purposes - Rogers further demonstrated how Defendants misused investors’ capital. (See id.

¶¶ 89-94.) From the Investment Period onward, Defendants spent over $2.4 million on nonAdvance business expenses and an additional $3.945 million on personal expenses. (Id. ¶¶ 91, 77.)

Notable amounts included over $1.8 million to American Express, payments to prior KrunchCash

investors, nearly $1 million to Hackman’s asset protection attorney (Kahan & Kligler LLP

(“K&K”)), private tuition for Hackman’s children, and payments for Porsche, BMW, and Volvo.

(See id. ¶¶ 91.) Hackman admitted that these were personal expenses. (Ex. 6 at 45:2–49:18.)

Notably, Hackman siphoned $650,000 to K&K on April 23, 2021—seven days after Pursuit sent

its initial attorney letter demanding transparency into the Advances. (Ex. 6 at 133:15–145:4, Ex.

27, Ex. 37 (Bank Excerpts 4/23/2021), see also Ex. 6 at 3:21; 134:1-137:24.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

19 of 32

20

vi. Missing Monies for Advances - Rogers next analyzed whether and to what extent Defendants had under-funded

Advances. (See id. ¶¶ 95-101.) The Pursuit and Signal Ledgers indicate $51.7 million funded to

the Resnick Firms and $43.2 million collected from those entities, i.e., $8.49 million net outflow.

(See id. ¶¶ 97.)5 Hackman represented that such monies were being funded to the Recipients for

Advances. (Ex. 21 at 61:4–62:3, 111:21–112:9.) And Hackman represented that the Resnick Firms

had received, and stolen, far more money than repaid. (Ex. 21 at 202:6-18, Ex. 1 at 329:4–330:13.) - The bank records, however, indicate that only $6.8 million—not $51.7 million—

was funded to the Maryland Recipients. (See id. ¶¶ 99.) The records also indicate that, contrary to

Hackman’s statements, Jonathan Resnick had repaid more capital than he received. (See id., (Ex.

21 at 202:6–18.) Thus, Hackman overstated—by many multiples—the cash funded to the

Maryland Firms and caused investors to invest capital never used for Advances. (See id. ¶¶ 101.)

vii. Sources of Payments to Investors - Finally, Rogers analyzed whether funding invested during the Investment Period

from Pursuit, Signal, and 1939 was used to repay previous and current KrunchCash investors. (See

id. ¶¶ 102-108.) Rogers concluded there were insufficient legitimate sources of funds—profits or

unrelated capital—to repay investors from the KrunchCash Entities bank accounts. (See id.) Thus,

Hackman necessarily used investor capital—not profits—to repay investors. (See id.)

H. The Forensic Analysis Demonstrates Several Varieties of Fraud - Rogers also performed a forensic analysis. (See id. ¶¶ 111-189.)

5 Such amounts are conservative because they do not include 1939’s investment. (See id.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

20 of 32

21

i. The KrunchCash Entities’ Records Meet the Red Flags of a Ponzi Scheme - Rogers explained that there are forensic definitions of a Ponzi scheme promulgated

by The Fraud Examiner Manual, 2020 U.S. Edition (the “Fraud Examiners Manual”) and by the

Securities and Exchange Commission (SEC). (See id. ¶¶ 112-120.) A Ponzi scheme is defined as:

A Ponzi scheme is generally defined as an illegal business practice

in which new investors’ money is used to make payments to earlier

investors The investment opportunity is typically presented with the

promise of uncommonly high returns. Everyone involved in

promoting the scheme pretends to represent a legitimate

organization, but little or no commercial activity takes place. The

Ponzi scheme usually unravels either when the operators keep all of

the proceeds for themselves or when the number of new investors

declines and dividends cannot be paid to investors. These scheme

usually run for a short period of time (e.g., one or two years),

although some Ponzi scheme had flourished for a decade or more.

In accounting terms, money paid to Ponzi investors is described as

income, but it is actually distribution of capital. Instead of receiving

investment profits, investors receive cash reserves.

(Id. ¶ 116 (citing the Fraud Examiners Manual §1.336).) - The Fraud Examiners Manual contains a test for “red flags” of a Ponzi scheme,

which Rogers opined were met: (1) 48% annualized returns “[s]ounds too good to be true,” (2) the

Ledgers indicating consistent repayment of claims constitute “[p]romises of low risk or high

returns,” (3) “[p]ressure to reinvest” indicated by Pursuit’s consistent reinvestment into alleged

new deployments into Advances, (4) litigation funding is generally considered a “[c]omplex

trading strateg[y]”, (5) there is “[l]ack of transparency or access” because Pursuit did not have

access to the end-Recipients, the lawsuits, or the KrunchCash bank records, and (6) Hackman’s

complete dominion over the entities constituted “[l]ack of separation of duties[.]” (Id. ¶ 117-118.) - Most significantly, the fact that “(1) investor funds are used to pay earlier investors

and (2) lack of profits requires increased investor funds,” as discussed above, warrants the

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

21 of 32

22

conclusion that Defendants met the forensic accounting definition of a Ponzi scheme. (See id. ¶¶

119-120.)

ii. The KrunchCash Entities’ Records Indicate False Entries, Churning, and

Double-Pledging - Rogers also continued analyzing the Ledgers, Settlement Sheets, and other data to

diagnose fraud. (Id. ¶¶ 121-172.) He identified three noteworthy fraudulent patterns: - First, in comparing the Pursuit and Signal Ledgers, Rogers observed that certain

names existed on each Ledger in near-identical names and during the same periods. (See id. ¶¶

126-146.) For example, “Jamshidy, Shiraz” was on the Pursuit Ledger, but “Jamshidy, Shirraz” –

the same name, but with an extra “r” – was on the Signal Ledger. (See id.) Elsewhere, the two

ledgers contained the same name, but inverted a hyphenated last name (e.g., “Whitfield-Welborn”

versus “Welborn-Whitfield”). (See id. ¶¶ 130.) Rogers thus tested the data for entries with 95%

(but less than 100%) similarity, i.e., “fuzzy” entries. (See id.) Rogers identified 866 fuzzy entries,

and concluded such entries were significant and not random because they were concentrated on

seven days. (See id ¶¶ 137.) Because KrunchCash could not have made two advances secured by

the same client, it necessarily means that Hackman created false entries within the Ledgers. (See

id. ¶¶ 145-146 (citing the Fraud Examiners Manual § 19.05).) - Second, Rogers continued his analysis of apparent “churning” of claims, wherein

Hackman sold claims back-and-forth between the Pursuit and Signal Ledgers. (See id. ¶¶ 121-125,

147-164.) “Churning” is defined as:

… the excessive trading of a customer account to generate

commissions while disregarding the customer’s interests.

Specifically, churning occurs when an investment professional

excessively trades an account for the purpose of increasing their

commissions instead of furthering the customer’s investment goals.

(Id. ¶ 147 (citing the Fraud Examiners’ Manual § 2.561).)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

22 of 32

23 - Per the Fraud Examiners’ Manual, churning is determined by two metrics:

“turnover” and “cost-to-equity” ratios. (Id. ¶¶ 152.) Both are met. 2,749 individual names appeared

on both Ledgers, with approximately half overlapping simultaneously. (See id. ¶¶ 153.) As a result

of Defendants’ selling collateral back-and-forth, the investors paid multiple fees to Hackman

despite there being no economic activity between KrunchCash and the end-Recipient—i.e., no

additional cash was paid to the firm. (See id. ¶¶ 153-156.) The “turnover” was extremely high.

(See id.) - The “cost-to-equity” was even more staggering. (See id. ¶¶ 157-164.) Cost-toequity measures the ratio of cost (fees to Hackman) versus equity (the value from the claims). (See

id.) Rogers measured this in two ways. For one, KrunchCash, in fact, funded $6.8 million to the

Resnick Firms and the total repaid was $5.2 million, i.e., a $1.62 million loss during the Investment

Period. (See id. ¶¶ 158.) Defendants’ profit-share—created through Hackman’s selling claims

back-and-forth—however, was over $2 million for Pursuit alone (and additional including Signal).

(Id. ¶¶ 159.) Thus, the cost-to-equity ratio on these metrics was $2 million versus a $1.2 million

loss, i.e., a cost-to-equity of infinity. (See id. ¶¶ 161-162.) - More conservatively, Rogers measured the same $2 million profits against the $6.8

deployed to the Resnick Firms or the $5.2 million collected from the Resnick Firms. (See id. ¶¶

161-162.) This resulted in a cost-to-equity ratio of 30.44% or 39.27%. (Id.) Given that Defendants’

profit-share was to be set at 12% (calculated as half of one 24% “Use Fee”) and payable only if

the investment succeeded, a cost-to-equity ratio of 30.44%–39.27% is nonsensical. (See id. ¶¶ 162-

164.) Thus, Defendants’ behavior meets the forensic test of churning. (See id.) - Third, Rogers’ fraud examination identified fraudulent dates that could not have

existed. (See id. ¶¶ 165-172.) The Ledgers that Hackman presented indicate a date a claim—an

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

23 of 32

24

injury lawsuit—began and ended. (See id.) Rogers compared the data in the Ledgers to the date in

the Settlement Sheets—i.e., the actual data—and determined that the beginning and end dates in

the Ledgers overstated that duration and existence of claims. (See id. ¶¶ 170-172.) - For instance, of the claims where Rogers had complete data, over 70% of such

entries reflected start dates on the Pursuit or Signal Ledger that predated the date of accident

reflected on the Settlement Sheets. (See id. ¶¶ 170.) This is impossible. In the case of Perry Resnick,

the start date on Hackman’s Ledgers sometimes pre-dated Perry Resnick’s formation of his law

firm or admittance to the practice of law. (Ex. 23 at 85:16–90:16 (discussing example of “claim”

on Pursuit Ledger dated March 1, 2016, which was prior to Perry Resnick’s practice of law or

formation of his law firm), Ex. 52 (Email Hackman to Perry Resnick 6/27/2019), see Ex. 23 at

85:16-86:7).) This too was impossible. (Ex. 23 at 13:15-15:20, 136:10-137:25.) - The same is true for the end of the end-date of the claim. In numerous instances,

Hackman reflected funded dates on Pursuit’s Ledger after the date—as reflected on the Settlement

Sheet—that the lawsuit as resolved and paid. (See Ex. 10 ¶¶ 165-172; Ex. 23 at 129:9–130:5,

41:14–23, Ex. 22 at 92:23–93:5, Ex. 36-1–36-5.) Jonathan and Perry Resnick testified this was

impossible, as well. (See id.) - Hackman’s actions (i) inflated claim values, (ii) created multiple false claims that

did not reflect fundings to the Resnick Firms, and (iii) created irreconcilable double-pledging

concerns.6

6 While not pertinent to this action, Hackman’s falsely inflating the Resnicks’ debts better explains

Hackman’s fraud against the Resnick Firms and in the Default Actions. There is evidence that, as

part of Hackman’s coverup, Hackman (i) created and submitted false ledgers with false

information as to the monies funded to the Resnick Firms, (ii) fraudulently backdated contracts

with the Resnick Firms, and (iii) for the claims reflected as being handled by Perry Resnick,

reflected claims that predated Perry’s formation of his law firm or admittance to the practice of

law, or after Perry stopped practicing law because he was incapacitated and too ill to practice law

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

24 of 32

25 - The process at the Maryland Law Firms was to obtain an advance from KrunchCash

for every new case, resulting in all incoming cases being routinely encumbered. (Ex. 57, (Norfolk

Dep. 11/22/2024) at 88:20-21, 89:4-5, 111:11.)

iii. Defendants Extracted Excess Capital from Pursuit Based on False LB Pharma

Ledger Entries - Finally, Rogers concluded that Hackman extracted millions in extra capital from

Pursuit based on false data of the amounts deployed to LB Pharma. (See id ¶¶ 173-189.) Pursuit

reinvested existing capital to LB Pharma and also invested $1.5 million and $3.8 million in cash

in July and October 2018, respectively. (See id. ¶¶ 177.) The Ledger indicates that full tranches

funded to LB Pharma was successfully repaid on certain dates, that Hackman was due a fee, and

that new capital was needed to be deployed into new tranches. (See id. ¶¶ 175-178.) - In fact, the actual LB Pharma transactions, indicate that what were reflected cashflows on the Ledgers were not so. (See id. ¶¶ 179-181.) In the Default Actions, Hackman admitted

that LB Pharma did not actually fully repay tranches; rather, from the very first tranche, there were

shortfalls that Defendants resolved by “rolling forward” prior unsuccessful tranches into new

tranches. (See id.) Hackman, however, reflected the old tranches as repaid and the new tranches as

requiring new cash capital. (See id.) - Rogers explained that, economically, Hackman drew capital from Pursuit that was

never actually fund to LB Pharma. (See id. ¶¶ 181-183.) Rogers quantified the overfunding, which

included $621,071, $925,185, $1.165 million, and over $3 million in each of August, September,

October, and December 2018, respectively. (Id. ¶ 183.) These transactions created an everin February/March 2019. (Ex. 23 at 128:9–130:5, 41:14–23, 143:8–23, 139:5–7, 85:16–90:16, Ex.

22 at 145:18–148:4, Ex. 21 at 172:21–19.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

25 of 32

26

increasing difference between the cash Pursuit dedicated versus the monies funded; with Hackman

thus collecting millions from Pursuit it did not use as represented. (See id.) - The October 2018 funding is particularly notable. (See id. ¶¶ 185-189.) The Ledger

indicates that approximately $4 million was to be funded to LB Pharma in October, and that Pursuit

wired $3.8 million in new capital for such purpose. (See id. ¶ 185.) In fact, however, only $2.127

million was funded to LB Pharma. (Id.) Hackman admitted that $4 million was not sent to LB

Pharma. (Ex. 1 at 335:23-336:4 (“We didn’t actually send $4 million.”).) - October 2018 was an important month. As can now be deciphered, Pursuit infused

$3.8 million within days of Defendants’ payment of a substantial sum to an outgoing investor. (Ex.

1 at 146:16–153:23 (Q: That was the final settlement payment that KrunchCash owed to Coach

house; right? A: Uh-huh.), Ex. 39 (Bank Excerpts 10/12/2018); Ex. 6 at 151:20-152:22

(authenticating Exhibit 39).) - Also in October 2018, Hackman attempted to re-sell LB Pharma receivables to

Signal for $50 million, which Signal declined. (Ex. 21 at 219:20–232:6, Ex. 40 (Term Sheet to

Signal 11/2018); Ex. 21 at 229:4-229:20 (authenticating Exhibit 40); Ex. 41 (Email to Signal

4/19/2019); Ex. 21 at 234:10-235:9 (authenticating Exhibit 41); Ex. 42 (Spreadsheet to Signal

4/2019); Ex. 21 at 235:10-236:14 (authenticating Exhibit 42); Ex. 1 at 190:1–216:22, Ex. 43

(Email to Signal 10/10/2018); Ex. 4 at 190:10-24 (authenticating Exhibit 43); Ex. 44 (Email to

Signal 12/17/2018); Ex. 4 at 195:8-197:19 (authenticating Exhibit 44); Ex. 45 (Spreadsheet to

Signal 12/17/2018); Ex. 4 at 195:8-197:19 (authenticating Exhibit 45); Ex. 46 (Email to Signal

1/8/2019); Ex. 4 at 198:21-199:6 (authenticating Exhibit 46); Ex. 47 (Email to Signal 1/23/2019);

Ex. 4 at 202:16-203:6 (authenticating Exhibit 47); Ex. 48 (Term Sheet to Signal 12/2018); Ex. 4

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

26 of 32

27

at 211:12-23 (authenticating Exhibit 48).) As is now clear, Hackman’s Ponzi scheme crashed when

Hackman was unable to attract new capital to support the false profits. (Ex. 10 ¶¶ 112-120.)

I. Defendants Waive or Decline to Produce Categories of Information Defendants

Have No Financial Statements, and Refuse to Provide Tax Returns

a. Defendants Have No Financial Statements and Refuse Tax Returns - Defendants have vehemently opposed any inquiry into the finances of the

KrunchEntities. (Ex. 5 at 44:25–54:25 (Hackman “refus[ing] to answer the question” concerning

finances, claiming it was none of Pursuit’s business).) - In April 2024, Pursuit moved to compel production of the KrunchCash Entities’ tax

returns. (Doc. 421.) The Court denied Pursuit’s request without prejudice, but acknowledged the

possibility that tax returns might be the only available records reflecting Defendants’ financial

performance. (Doc. 511 at 12:05–12, 57:06–15.) - In deposition, Defendants confirmed they did not maintain balance sheets, profitand-loss statements, general ledgers, or other contemporaneous financial records against which to

test the veracity of the “Ledgers.” (Ex. 5 at 43:12–24, 50:6–53:23.) Pursuit renewed its request for

the tax returns, which the Court granted. (Doc. 645.) - When Defendants numerous times refused to comply (Doc. 693, 733), Pursuit

moved for contempt. (Doc. 740.) The Court granted that motion and struck Defendants’ answer

with an opportunity to cure were they to produce the entity tax returns. (Doc. 749.) - Following such order, Defendants produced redacted excerpts of tax returns for an

unknown entity for 2018-2020. (Ex. 49–51 (2018 Schedule 1120 (Unknown Entity), 2019

Schedule 1120 (Unknown Entity), 2020 Schedule 1120 (Unknown Entity).) Though Defendants

redacted the filer of such returns, the Schedule G indicates that the filer was owned by—and thus

cannot be—KrunchCash. (Ex. 49–51; Ex. 55 (Hackman Dep. 7/31/2025) at 108:24-109:18, 154:3-

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

27 of 32

28

16, 170:25-171:25 (authenticating 2018, 2019 and 2020 Schedule 1120).). Defendants explained

that that Defendants did not have the KrunchCash Entities’ returns in their possession. (Doc. 793

(Defendants “produc[ed] what they represent are the tax returns in their possession”).) The Court

found that Defendants purged the contempt. (Doc. 793.) - The redacted filer had, in each of 2018, 2019, and 2020, respectively, (1) losses of

$378,146, $381,621, and $856,160, (2) assets of $1,000, and (3) negative retained earnings of

$137,324, $570,431, and $1.8 million (Ex. 49–51.)

b. Defendants Waive the Right to Present Evidence on the NFL Profits - In December 2024, Defendants moved to quash a subpoena Pursuit served upon

American Express to obtain records concerning Hackman’s millions in expenses. (Doc. 626.)

Pursuit presented an affidavit from Rogers explaining that, as discussed above, there is a multimillion-dollar gap between Defendants’ expenses and legitimate sources—profits and capital—

such that Hackman used investor money for expenses. (Doc. 634 ¶¶ 8-10.) - On reply, Hackman maintained his excuse—that KC CA was a repository for

profits—and now attested, specifically, that:

In 2015, 2016 & 2017, unrelated to any investment funding provided

by [Pursuit], KrunchCash advanced funds to NFL players in the

NFL Class Concussion Litigation along with other investments. In

2017, KrunchCash began receiving profit distribution through May

2021, KrunchCash has received over $4.5M in distributed profits,

which was deposited into KC CA.

(Doc. 639 ¶ 7.) - Days later, Pursuit deposed Hackman, as representative of KC CA. Hackman was

unable to reconcile his claim of profits from the NFL Advances, testified that he could not recall

details of the purported NFL returns, and stated that to provide information concerning NFL

Advances that “I would have to go back into my record, for the umpteen millionth time.” (Ex. 1 at

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

28 of 32

29

64:18–102:4, 89:18–23.) Hackman did testify, however, that he maintained “spreadsheets” with

respect to the NFL Advances. (Id. at 69:2–8, 72:17–24, 74:18–75:15.) - In an attempt to understand Defendants’ apparent defense, Pursuit thus demanded

such spreadsheets and Defendants moved to quash. (Doc. 655.) At argument, Defendants

maintained their objection. (Doc. 735.) The Court gave Defendants the option to produce the

spreadsheets or waive the right to present evidence:

The Court: Let’s be clear, right? They are objecting to producing

this information [the NFL ledgers].

Mr. Fried [counsel for Pursuit]: Yes.

The Court: That means that if they try to introduce it at trial I will

exclude it.

Mr. Fried: If Your Honor is willing to make that ruling now?

The Court: Well, I assume that Ms. Roy [counsel for Defendants]

would understand that. Maybe I should ask you [to Ms. Roy]. I

always find this interesting dynamic when people are asking for

production of things. If they don’t produce it, and they object to

producing it, they can’t use it.

So, Ms. Roy, are you comfortable with the idea, on the record, that,

you know, when we get to trial or even Summary Judgment, if your

client wants to bring in evidence of some of this NFL income or the

like, I think I would be correct to prohibit that from coming in if you

have resisted discovery on it.

Ms. Roy: That’s correct. I believe that the NFL records would not

in any way effect the outcome of this litigation or my client’s claims.

The Court: Despite the fact that there is going to be an expert report

coming in, presumably, purporting to establish that there was no

apparent source, legitimate source for some of these expenditures,

your client might, as some point, want to say: Well, here is the

source and if you blocked discovery into them, I think you may be

precluded from doing that.

Ms. Roy: Again, within the contract Pursuit has already

acknowledged that KrunchCash has had other businesses and other

investors.

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

29 of 32

30

The Court: I get all that. I’m just saying: This is the real world. We

are at trial. You are about to ask Mr. Hackman on the stand to

explain what the source was for his, you know, using “X” funds to

do “Y” thing and if he is going to testify about this topic, you know,

whether it’s the NFL contracts or whatever, I might well preclude

him from doing that based on the position taken by Defendant that

this is all irrelevant.

It’s a two-way swinging door; right? It’s either in or it’s out. It

sounds to me like the Plaintiffs are only seeking it to potentially

respond to an affirmative argument that the defendant might make.

Before I make my decision on all of that, I just want to make sure

that you are aware that, at least presumptively, if I agree with the

Defendant on this and preclude them from getting it, that means I

will hold Defendant to the argument that the NFL revenues are

irrelevant, including at trial.

Ms. Roy: That’s correct.

The Court: Okay.

Mr. Fried: Okay, Your Honor. I would just ask that that winds up in

an Order somewhere.

The Court: That’s on the record.

(Doc. 735 at 30:4-32:11.) The Court so-ordered the stipulation on the record. (Doc. 717.)

J. Defendants Waive any Expert Report - On March 19, 2025, the Court so-ordered a final discovery stipulation. (Doc. 728.)

Whereas Pursuit agreed to a deadline to submit its expert report, which it did, “Defendants

waive[d] any expert report.” (Id. ¶ 7.)7 - Hackman testified repeatedly that he does not practice accounting or provide

accounting for the KrunchCash Entities. (Ex. 1 at 142:5–143 (“I am not a tax accountant”), 229:10-

17 (Q: And you never practiced [accounting] a day in your life? A: No.), 230:24-231:4 (no

7 Hackman testified that his counsel previously engaged an expert, but that such expert was

disengaged without any work product. (Ex. 6 at 44:4–23.)

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

30 of 32

31

accounting certification or professional licenses), 231:17–20 (Q: Would you consider the work

that you did for KrunchCash practicing any accounting? A: No.).)

K. Hackman is the Alter Ego of the KrunchCash Entities - Each of the KrunchCash Entities is owned, controlled, and operated by Hackman

without regard for corporate formalities and in a manner commingled with Hackman’s personal

finances. (See Ex. 1 (KC PCRD Dep. 7/17/2024) at 21:23–22:12; Ex. 2 (KC PCRD Dep. 1/8/2025)

at 10:1–19; Ex. 5 (Hackman Dep.) at 4:15-4:22; Ex. 6 (KC CA Dep. 1/17/2025) at 10:2–11:13.) - None of the KrunchCash Entities has an operating agreement, financial statement

or written policy. (Ex. 1 at 23:13–24:8.) Hackman is the manager of each KrunchCash Entity. (See

id. at 24:6–25:25, 47:6–21.) There are no written agreements among any of the Defendants. (See

id. at 25:2–26:4, 205:22–207:24.) KC PCRD never issued 1099s or K-1s to another Defendant or

to Pursuit. (Id. at 138:17–141:19.) KC PCRD’s sole member was KrunchCash, and Hackman has

stated he is sole member of KrunchCash. (See id. at 139:2–25.) - Hackman claims that the KrunchCash Entities’ finances were consolidated in one

tax return, which was consolidated with Hackman’s personal returns. (See id. at 142:13–147:25.)

Hackman unilaterally controls all books and records and bank accounts for the KrunchCash

Entities. (Ex. 5 (Hackman Dep. 1/9/2025) at 8:22–9:24, 43:12–24.) - Hackman admitted that he makes all decisions concerning the KrunchCash Entities

he wholly owns. (Ex. 6: 14:18-17:23 (“Is it fair to say you make all decisions concerning KC CA?

A: It’s fair to say that. Q: You don’t answer to anybody, right, Mr. Hackman? A” I do not answer

to anybody.”).) - All calculations and determinations of amounts owed to KrunchCash from the

Maryland Recipients were controlled by Hackman, who provided the figures for repayment and

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

31 of 32

32

issued instructions regarding settlement reconciliations and spreadsheets (Ex. 57 (Norfolk Dep.

11/22/2024) at 109:14-18, 113:15-17, 116:7-19, 117:1-19, 119:6, 120:14-15.) - The record is also rife with Hackman’s admissions that he did little to respect or

observe corporate formalities. (Ex. 6: 18:24-19:25 (confirming KC CA, KC PCRD, and

KrunchCash’s place of business is Hackman’s home).) - Hackman commingled all investors’ capital in the KrunchCash “cash management

account,” (Ex. 10 ¶¶67-72) and transferred millions to KC CA for personal uses, including for his

daughter’s high school and college tuition and payments for a family Porsche Macan and unknown

model Volvo. (Ex. 33; Ex. 1 at 76:22–79:21; Ex. 6 at 60:4-61:20). Hackman testified that, to the

extent the KrunchCash Entities made tax filings (which Hackman refuses to provide), they are

“consolidated” with Hackman’s personal returns. (Ex. 1 at 142:13–147:25.)

Dated: October 17, 2025

New York, NY

SLARSKEY LLC

By: /s/Evan Fried

Evan Fried

767 Third Ave., 14th Floor

New York, NY 10017

Counsel for Plaintiff

FILED: NEW YORK COUNTY CLERK 10/17/2025 05:34 PM INDEX NO. 651070/2022

NYSCEF DOC. NO. 814 RECEIVED NYSCEF: 10/17/2025

32 of 32